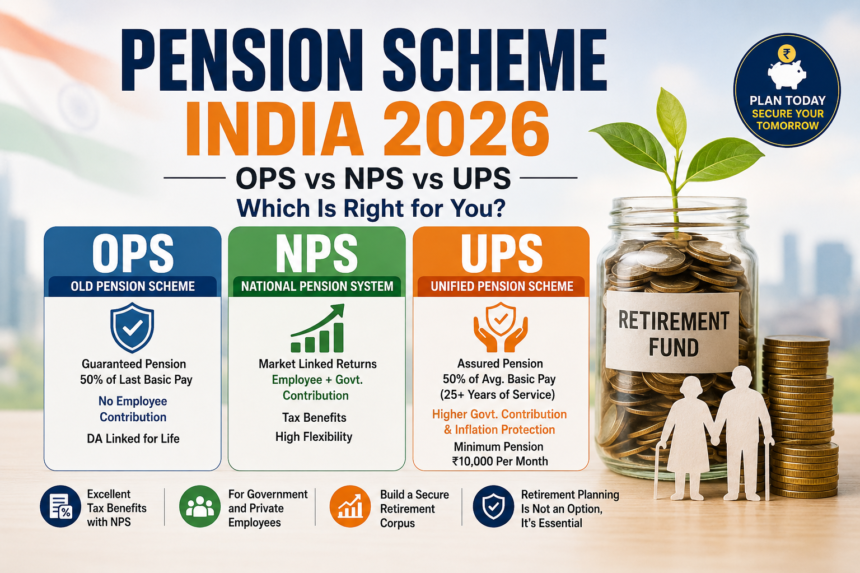

Pension Scheme India 2026, The debate over India’s pension system has moved from academic discussions to one of the most politically charged topics in Indian public policy. The Old Pension Scheme (OPS), which provided guaranteed retirement income to government employees, was discontinued for new central government employees from 2004, replaced by the National Pension System (NPS). Then in 2025, the government introduced the Unified Pension Scheme (UPS) — a hybrid option that attempts to address the legitimate concerns of government employees without fully reverting to OPS.

For private sector employees, NPS remains a powerful and tax-efficient retirement savings tool that few fully utilise. This comprehensive guide explains all three pension systems in plain language, compares them honestly, and helps you understand which is right for your situation in 2026.

Old Pension Scheme (OPS): What It Was and Why It Was Discontinued

What OPS Provided

The Old Pension Scheme guaranteed central government employees a defined benefit pension — 50% of the last drawn basic pay, revised upward with every Dearness Allowance (DA) revision. An employee who retired with a basic pay of Rs 60,000 would receive Rs 30,000 per month as pension for life, with the amount increasing automatically as DA increases.

Additionally, OPS provided family pension (typically 30% of last basic pay to spouse after employee’s death), gratuity, and other terminal benefits. Importantly, employees contributed nothing from their own salary to OPS — the entire pension liability was borne by the government.

Why OPS Was Discontinued

OPS was discontinued because its unfunded liability — pension commitments with no dedicated fund behind them — was growing at an unsustainable rate. With 5.4% of India’s GDP potentially going toward government pension payments by 2040 under OPS, the fiscal mathematics were simply not viable. NPS replaced OPS to create a funded, actuarially sound system.

National Pension System (NPS): How It Works

Pension Scheme India 2026, NPS is a market-linked, contribution-based pension system. Both the employee and government contribute a percentage of salary (currently employee: 10% of basic pay + DA; government: 14%). The combined contribution is invested in a mix of equities, government bonds, and corporate bonds chosen by the subscriber, and the accumulated corpus at retirement determines the pension.

NPS Returns and Market Risk

NPS returns depend on market performance — unlike OPS which was guaranteed regardless of market conditions. Historical NPS returns have been 9-12% per annum over the long term for equity-heavy allocations. However, short-term market volatility affects the corpus, and an employee retiring during a market downturn receives less than one retiring during a bull market — a fundamental fairness concern that led to the introduction of UPS.

NPS Tax Benefits — Extremely Attractive for Private Employees

For private sector employees who choose NPS voluntarily, the tax benefits are exceptional:

- Section 80CCD(1): Up to 10% of salary contribution deductible — within the Rs 1.5 lakh 80C limit

- Section 80CCD(1B): Additional Rs 50,000 deduction over and above the Rs 1.5 lakh 80C limit — this is a uniquely valuable additional benefit

- Section 80CCD(2): Employer NPS contribution up to 14% of salary fully deductible — not included in the Rs 1.5 lakh limit

- At retirement: 60% of corpus can be withdrawn tax-free; 40% must be used to buy annuity

Unified Pension Scheme (UPS): The New Middle Path

Pension Scheme India 2026, The Unified Pension Scheme, announced in 2025 and implemented from April 2025, is available to central government employees as an alternative to NPS. It represents the government’s attempt to address the legitimate grievances of NPS employees without fully reverting to the fiscally unsustainable OPS.

Key UPS Features

- Assured pension: 50% of average basic pay of last 12 months before retirement — for those with 25+ years of service

- Proportionate pension: For those with 10-25 years of service — proportionate assured pension

- Minimum pension: Rs 10,000 per month guaranteed for those with at least 10 years of service

- Family pension: 60% of employee’s pension payable to family on employee’s death

- Inflation protection: DA linked to industrial workers’ Consumer Price Index — same as for OPS

- Employee contribution: 10% of basic pay + DA (same as NPS)

- Government contribution: 18.5% (increased from 14% under NPS — the higher government contribution funds the assured element)

UPS vs NPS vs OPS: The Numbers

For a government employee retiring with basic pay of Rs 60,000 after 25+ years of service:

- OPS: Rs 30,000 per month (50% of Rs 60,000) — guaranteed, no employee contribution

- UPS: Rs 30,000 per month (50% of Rs 60,000) — guaranteed, but employee contributed 10% throughout service

- NPS: Depends on market returns — potentially Rs 30,000-60,000+ per month with good returns; potentially less with poor returns

NPS for Private Sector Employees: A Powerful Retirement Tool

Pension Scheme India 2026, While the OPS vs UPS debate is primarily relevant for government employees, NPS is available to all Indian citizens including private sector employees. For private sector employees, NPS is one of the most tax-efficient retirement savings vehicles available.

Who Should Consider NPS as a Private Employee?

- Anyone who has maxed out their 80C limit (Rs 1.5 lakh) and wants additional tax deduction — the Rs 50,000 extra deduction under 80CCD(1B) is uniquely valuable

- Anyone in a high tax bracket (30%) where the tax saving is most valuable

- Young professionals with 25+ years to retirement — compounding over long periods works powerfully in NPS

- Those whose employer offers NPS matching — employer contribution is essentially free retirement savings

NPS Investment Choices

NPS offers different fund managers (SBI, LIC, HDFC, ICICI, Kotak, Aditya Birla, UTI) and asset class allocations:

- Tier 1 (mandatory for tax benefit): Lock-in until age 60; partial withdrawals allowed for specific purposes after 3 years

- Tier 2 (voluntary, no tax benefit): Fully liquid — withdraw anytime; no mandatory annuity purchase

- Auto choice: Automatically reduces equity allocation as you approach retirement — convenient but less flexible

- Active choice: You decide equity vs debt allocation — better for those comfortable with investment decisions

How to Open an NPS Account in 2026

- Online: Visit enps.nsdl.com or proteantech.in — complete registration with PAN, Aadhaar, and bank details

- Through employer: Many private companies offer NPS through their payroll system

- Through banks: Most banks and post offices can open NPS accounts with physical KYC

- Minimum contribution: Rs 500 per contribution; Rs 1,000 per year minimum

Which Pension Scheme Is Best? The Verdict

For Government Employees Joining Now (Central Government)

Choose UPS over NPS if retirement security is your priority and you are willing to accept the constraint of assured (but not market-upside) returns. Choose NPS if you believe you can actively manage your investments and are comfortable with market-linked outcomes that could exceed the UPS assured amount.

For State Government Employees

Several states (Rajasthan, Chhattisgarh, Jharkhand, Punjab, Himachal Pradesh) have reverted to OPS. If you are a state government employee in these states, OPS applies. In UPS states, the central Unified Pension Scheme (UPS) framework applies. In remaining NPS states, NPS continues.

For Private Sector Employees

NPS is genuinely excellent for tax efficiency. Open a Tier 1 NPS account, contribute Rs 50,000 per year to claim the additional 80CCD(1B) deduction, and leave the rest invested. Over a 25-30-year career, the combination of tax savings and compounding creates substantial retirement wealth.

Read More: Home Loan Interest Rate India 2026 Lowest: Best Banks & EMI Guide for Buyers

Conclusion

Pension Scheme India 2026, India’s pension debate is ultimately about one fundamental truth: the government of India cannot afford to provide generous defined benefit pensions to all its employees, and private sector employees have no government pension at all. Taking responsibility for your own retirement security — through NPS, PPF, mutual funds, or a combination — is not just advisable. It is essential.

Taza Newsz covers personal finance, pension policy, retirement planning, and tax guidance for Indian employees. Follow us for the latest on pension scheme changes, NPS returns, and retirement planning advice.