ITR Filing AY 2026-27, Filing an Income Tax Return (ITR) early is often considered a smart financial habit. It helps taxpayers avoid last-minute stress, receive refunds sooner, and stay compliant with tax regulations. However, for Assessment Year (AY) 2026-27, thousands of early filers may find themselves in an unexpected situation—having to revise their returns after submission.

Let’s explore why revised returns are becoming more common, the timelines taxpayers need to know, and how individuals can avoid unnecessary corrections.

The Rising Trend of Revised Income Tax Returns

In recent years, the number of taxpayers revising their returns has steadily increased. This trend is closely linked to the government’s enhanced ability to gather and process financial data from various institutions.

What does this mean for taxpayers?

Simply put, information that may not have appeared in official tax records when a return was initially filed could be added later. As a result, taxpayers often discover missing income details or transaction records after submission, forcing them to revise their returns to maintain accuracy.

It’s a bit like completing a jigsaw puzzle before all the pieces arrive. Once the missing pieces show up, the picture changes—and so must the tax return.

How Advanced Financial Reporting Is Changing Tax Compliance

ITR Filing AY 2026-27, The Income Tax Department’s reporting systems have evolved significantly over the past few years. Today, taxpayers are monitored through a sophisticated network of financial reporting mechanisms that capture a wide range of transactions.

These include:

- Salary income

- Interest earned from banks and deposits

- Dividend income

- Mutual fund investments

- Stock market transactions

- Property purchases and sales

- Foreign remittances

- High-value expenditures

Most of this information is reported directly by banks, employers, financial institutions, brokers, and other third-party entities.

Because these reports continue to be updated even after the financial year ends, taxpayers who file their returns too early may unknowingly submit incomplete information.

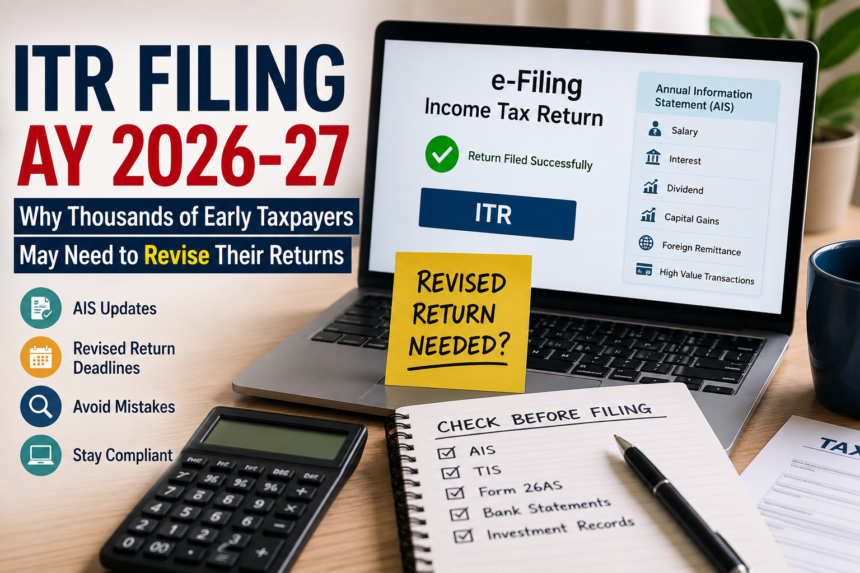

Understanding the Role of the Annual Information Statement (AIS)

One of the most important documents in the modern tax filing process is the Annual Information Statement (AIS).

The AIS acts as a comprehensive financial report card. It provides taxpayers with a consolidated view of various income sources and financial transactions reported to the Income Tax Department.

The statement includes data from:

- Employers

- Banks

- Mutual fund companies

- Stockbrokers

- Property registrars

- Foreign exchange service providers

While AIS has made tax filing more transparent, it is not always fully populated immediately after the financial year ends.

This creates a significant challenge for early filers.

Why Early Filers Are More Vulnerable to Errors

ITR Filing AY 2026-27, Many taxpayers rush to file returns as soon as the portal opens. While this may seem efficient, it can sometimes backfire.

Why?

Because employers, banks, and other reporting entities often complete their final data submissions weeks or months later.

For example:

- Fourth-quarter TDS filings may still be pending.

- Interest income updates may not yet appear.

- Capital gains data may be incomplete.

- Dividend information may be added later.

When new entries eventually appear in AIS, taxpayers may realize that their originally filed return no longer reflects complete financial information.

At that point, filing a revised return becomes necessary.

AIS and TIS Are Dynamic Documents, Not Fixed Records

Many taxpayers assume that once they download their AIS or Taxpayer Information Summary (TIS), the information remains unchanged.

That assumption can be costly.

Both AIS and TIS are dynamic documents. This means they can be updated continuously as new information is received from reporting entities.

Imagine checking a live cricket score before the match is over. The score you see at one moment may look completely different an hour later.

Similarly, the financial data visible in AIS today may not be identical a few weeks later.

This ongoing evolution is one of the primary reasons revised returns have become more common.

Technology-Driven Scrutiny Is Increasing Compliance Pressure

ITR Filing AY 2026-27, The Income Tax Department has significantly strengthened its data analytics capabilities.

Modern tax administration now relies heavily on:

Automated Data Matching

Advanced systems compare taxpayer disclosures against information received from third parties.

Faceless Assessment Processes

Digital scrutiny mechanisms operate without physical interaction, reducing human intervention and increasing efficiency.

AI-Powered Risk Detection

Sophisticated algorithms can identify discrepancies, omissions, and inconsistencies with remarkable accuracy.

As a result, even small mismatches between reported income and official records can be detected automatically.

This encourages taxpayers to proactively revise returns rather than wait for notices from the department.

Small Mistakes Can Trigger Big Consequences

Many taxpayers assume that only major discrepancies attract attention.

That’s no longer the case.

Even minor differences involving:

- Interest income

- Dividend receipts

- Capital gains calculations

- TDS credits

- Foreign remittances

can trigger alerts within the department’s analytics systems.

Think of these systems as financial radar. Even small deviations can appear on the screen.

Consequently, taxpayers increasingly prefer voluntary corrections through revised returns rather than dealing with future compliance issues.

Revised Return Deadline for AY 2026-27

Taxpayers should be aware of the timelines available for correcting errors.

For AY 2026-27, returns continue to be governed by the provisions of the Income Tax Act, 1961, despite the implementation of the Income Tax Act, 2025 from April 1, 2026.

Under Section 139(5), taxpayers can file a revised return:

- Up to December 31, 2026, or

- Before the completion of assessment,

whichever occurs earlier.

This provision allows taxpayers to rectify genuine omissions, incorrect disclosures, or reporting mistakes.

Proposed Extension Under the Finance Bill 2026

ITR Filing AY 2026-27, The Finance Bill 2026 proposes additional flexibility for taxpayers.

If approved, the revised return filing window may be extended until March 31, 2027.

However, there is an important catch.

Returns revised after December 2026 may attract a prescribed fee.

While this extended timeline offers relief, taxpayers should not view it as an excuse for delayed compliance. Early accuracy remains the most efficient approach.

What Happens After the Revision Window Closes?

Even after the revised return deadline expires, taxpayers may still have an opportunity to correct errors.

Section 139(8A) allows the filing of an Updated Return.

This option remains available for up to 48 months from the end of the relevant assessment year.

However, there is a trade-off.

Updated returns generally involve:

- Additional tax payments

- Interest charges

- Potential penalties

Therefore, relying on updated returns should be considered a last resort rather than a routine strategy.

How Taxpayers Can Avoid Filing Revised Returns

The simplest solution is careful preparation before filing.

Experts recommend conducting a thorough reconciliation exercise before submitting the return.

Check AIS Thoroughly

Review every entry in your Annual Information Statement.

Verify the Taxpayer Information Summary (TIS)

Ensure the summarized figures match your records.

Cross-Check Form 26AS

Confirm that all TDS credits and tax payments have be correctly reflect.

Review Supporting Documents

Compare tax records against:

- Form 16

- Bank statements

- Fixed deposit interest certificates

- Dividend statements

- Broker reports

- Capital gains statements

Report Errors Promptly

If incorrect information appears in AIS, use the “Report Incorrect Information” feature available on the income tax portal.

Special Attention Required for Taxpayers with Multiple Income Sources

ITR Filing AY 2026-27, Individuals with complex financial profiles face a higher risk of omissions.

This includes taxpayers who have:

- Multiple employers

- Stock market investments

- Mutual fund transactions

- Rental income

- Foreign assets

- Overseas remittances

- Capital gains from property sales

For such individuals, thorough verification is not optional—it is essential.

The more income streams you have, the more carefully you should reconcile your records before filing.

Why Accuracy Beats Speed Every Time

Many taxpayers focus on being among the first to file.

But when it comes to tax compliance, speed is not always an advantage.

A carefully prepared return filed slightly later is often far better than an early return that requires multiple revisions.

Think of it as building a house. A strong foundation takes time, but it prevents future repairs.

The same principle applies to tax filing.

Taking a few extra days to verify information can save months of complications later.

Read More: Pension Tax Rules AY 2026-27: Key Differences Between Pension and Family Pension

Conclusion

ITR Filing AY 2026-27, The increasing number of revised Income Tax Returns for AY 2026-27 reflects the growing sophistication of India’s tax reporting ecosystem. With the Annual Information Statement, Taxpayer Information Summary, and advanced analytics systems continuously capturing and updating financial data, taxpayers face greater pressure to ensure complete accuracy in their filings.

While revised and updated return provisions provide valuable opportunities to correct mistakes, they should ideally serve as safety nets rather than standard practice. Taxpayers who carefully reconcile AIS, TIS, Form 26AS, and their personal financial records before filing can significantly reduce the likelihood of future corrections and scrutiny.