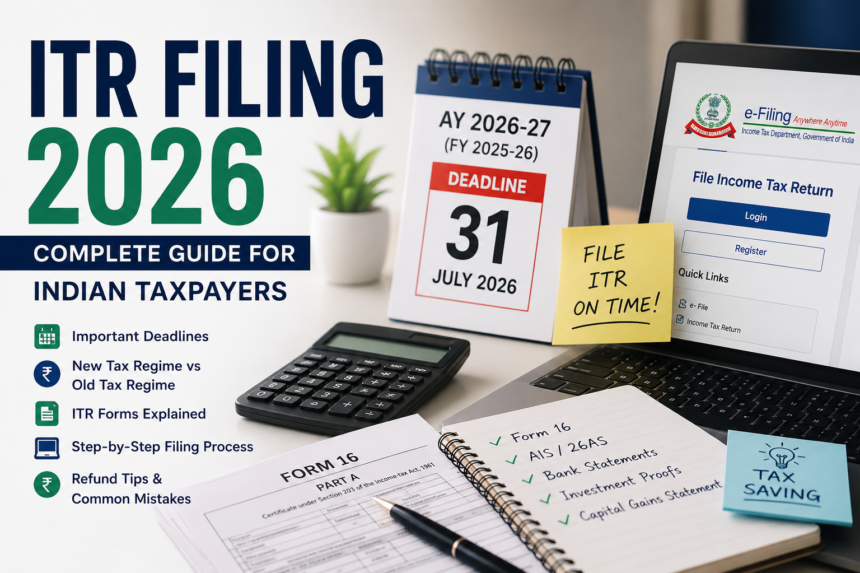

Every year, as the July 31 deadline for Income Tax Return (ITR) filing approaches, millions of Indian taxpayers scramble to gather documents, choose the right form, and navigate the Income Tax portal. The 2026 filing season (Assessment Year 2026-27, for income earned in Financial Year 2025-26) comes with important changes — the new tax regime has been significantly sweetened by Budget 2026, the Income Tax portal has been upgraded, and the government is pushing more taxpayers toward the simplified new regime.

Whether you are filing your ITR for the first time, switching from the old regime to the new, or dealing with a specific situation like freelance income or capital gains, this comprehensive guide covers everything you need to know for smooth, accurate, and timely ITR filing in 2026.

ITR Filing 2026: Key Deadlines

- July 31, 2026: Last date for individuals, HUF, and non-corporate taxpayers who do not require audit

- October 31, 2026: Last date for taxpayers requiring audit (businesses with turnover above specified limits)

- November 30, 2026: Last date for taxpayers with international transactions requiring transfer pricing report

- December 31, 2026: Last date for filing belated returns (after July 31 deadline, with late fee)

Filing after July 31 but before December 31 attracts a late fee of Rs 1,000 (for income up to Rs 5 lakh) or Rs 5,000 (for income above Rs 5 lakh). Always file on time — there is no extension unless the government announces one.

New Tax Regime vs Old Tax Regime 2026: Which Should You Choose?

This is the most important decision for most individual taxpayers in 2026. Budget 2026 has made the new tax regime significantly more attractive — the zero-tax threshold has been raised to Rs 12 lakh (with rebate), and slabs have been revised. But the old regime still makes sense for those with significant deductions.

New Tax Regime 2026: Updated Slabs

- Up to Rs 4 lakh: 0%

- Rs 4-8 lakh: 5%

- Rs 8-12 lakh: 10%

- Rs 12-16 lakh: 15%

- Rs 16-20 lakh: 20%

- Rs 20-24 lakh: 25%

- Above Rs 24 lakh: 30%

- Section 87A rebate: Zero tax for income up to Rs 12 lakh

- Standard deduction (salaried): Rs 1,00,000 (raised from Rs 75,000)

When New Regime Is Better

The new regime is mathematically superior for taxpayers who have limited deductions. If your total deductions under the old regime (80C, 80D, HRA, home loan interest, NPS) add up to less than approximately Rs 4-5 lakh, the new regime will result in lower tax. For most salaried individuals with income up to Rs 12 lakh and standard deduction plus basic investments, the new regime saves money.

When Old Regime Is Still Worth It

If you have a large home loan (substantial interest deduction under Section 24B), high HRA (renting in a metro city), maximum 80C investments (Rs 1.5 lakh), 80D health insurance (Rs 25,000-50,000), NPS employer contribution, and other deductions totalling Rs 5 lakh or more — calculate your tax under both regimes. The old regime may still save more.

Related: Home Loan Interest Rate India 2026: How the New Tax Regime Changes Your Calculation — Taza Newsz

Which ITR Form Should You File?

- ITR-1 (Sahaj): For resident individuals with salary/pension income up to Rs 50 lakh and one house property. Cannot be used if you have capital gains, business income, or foreign assets

- ITR-2: For individuals/HUF with capital gains, multiple house properties, foreign income, director of company, or income above Rs 50 lakh. Cannot be used if you have business income

- ITR-3: For individuals/HUF with business income or income from profession (including freelancers and self-employed)

- ITR-4 (Sugam): For individuals/HUF/firms using presumptive taxation scheme — businesses with turnover up to Rs 2 crore or professionals with gross receipts up to Rs 50 lakh

- ITR-5, 6, 7: For firms, companies, trusts — not for individuals

Step-by-Step Guide to Filing ITR Online in 2026

Step 1: Gather Required Documents

- Form 16 (from employer — shows salary and TDS)

- Form 26AS and Annual Information Statement (AIS) — download from Income Tax portal

- Bank statements for all accounts

- Investment proofs (80C, 80D, NPS, etc.)

- Capital gains statements from broker/mutual fund

- Rental income details (if applicable)

- Home loan certificate (principal and interest breakdown)

Step 2: Check Form 26AS and AIS

Before filing, always download and verify your Form 26AS (Tax Credit Statement) and Annual Information Statement from the Income Tax portal (incometax.gov.in). These documents show all TDS deducted on your behalf and all financial transactions registered against your PAN. Any discrepancy must be resolved before filing.

Step 3: Calculate Tax and Choose Regime

Calculate your tax liability under both old and new regimes using the IT department’s Tax Calculator on the portal, or use a reputed CA or tax filing service. Choose the regime that results in lower tax — you can change your choice each year.

Step 4: File on the Income Tax Portal

Log in to incometax.gov.in with your PAN and password. Navigate to e-File > File Income Tax Return. Select Assessment Year 2026-27, filing status (Original), and the correct ITR form. Fill the form using pre-filled data (the portal now pre-fills significant data from Form 26AS and AIS) and add any additional details.

Step 5: Verify Your ITR

After filing, your return must be verified within 30 days. The easiest method is e-verification using Aadhaar OTP — takes 2 minutes. Alternatively, verify through net banking, DSC (Digital Signature Certificate), or by sending a signed physical ITR-V to CPC Bengaluru by post.

Related: 8th Pay Commission India 2026: How Government Salary Changes Affect Your ITR — Taza Newsz

How to Get Your Income Tax Refund Faster in 2026

- Link PAN with Aadhaar — mandatory; refunds are blocked without this

- Validate your bank account on the IT portal — pre-validate your refund bank account

- File early — refunds are processed faster for early filers; July rush creates delays

- Check AIS carefully — discrepancies between your return and AIS trigger manual scrutiny, delaying refunds

- File error-free — incorrect TAN of employer, wrong bank account, or arithmetical errors cause refund delays

- Track refund status at tin.tin.nsdl.com — enter PAN and assessment year

Common ITR Filing Mistakes to Avoid

- Not filing if income is below taxable limit — filing is mandatory if turnover/receipts exceed Rs 60 lakh, or if specific conditions met (foreign travel spending, deposits above thresholds, etc.)

- Wrong ITR form — using ITR-1 when you have capital gains income is the most common error

- Not declaring all income — bank interest, dividend income, capital gains from mutual funds and shares must all be declared

- Not verifying within 30 days — unverified ITRs are treated as if not filed

- Ignoring AIS and Form 26AS — the IT department cross-checks your return against this data; discrepancies invite notices

Should You Use a CA or File Yourself?

For simple cases — salaried individuals with Form 16, standard deductions, and no capital gains or business income — filing yourself on the IT portal or through apps like ClearTax, H&R Block India, or myITreturn is perfectly feasible and saves the CA fee. For complex cases — business income, significant capital gains, foreign income, multiple properties, or high-value transactions — a CA or tax professional is strongly recommended.

Read More: New Income Tax Act: Key Changes, Benefits & What It Means for You

Conclusion

The ITR Filing 2026 brings good news for most Indian taxpayers — the new regime’s enhanced benefits mean lower taxes for a wider population. The key is to file on time, declare all income honestly, and verify your return promptly. Do not wait until July 30 to start — gather documents now, run the old vs new regime comparison, and file at least two weeks before the deadline.

Taza Newsz publishes ITR filing guides, tax policy updates, and Income Tax news throughout the filing season. Follow us for step-by-step assistance with every major ITR filing deadline.