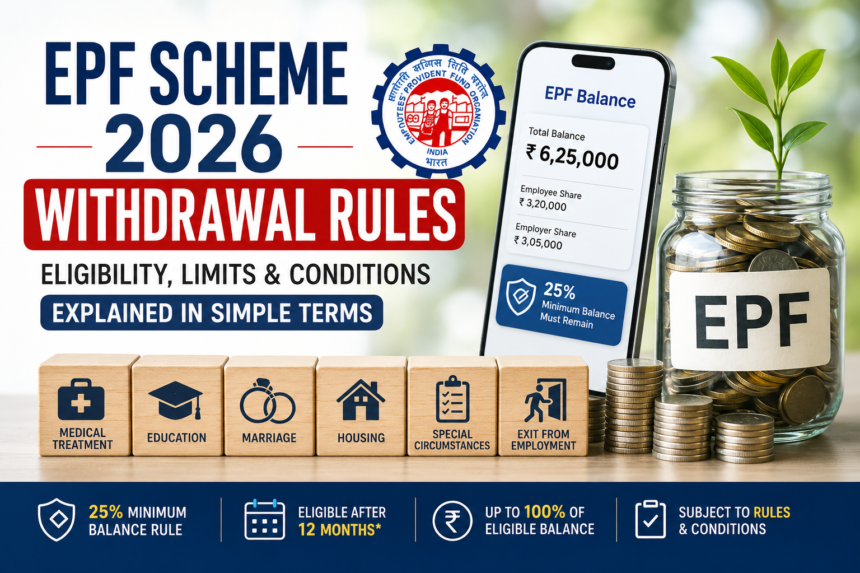

EPF Scheme 2026 Withdrawal Rules, India’s retirement savings system has entered a new chapter. The EPF Scheme 2026 is now in focus, and for millions of salaried employees, one question stands front and center: what exactly has changed in EPF withdrawal rules? If you have ever looked at your provident fund balance and wondered when you can use it, how much you can take out, and what conditions apply, this revised framework matters a lot.

The new rules, which came into effect on 29 June, replace the old EPF Scheme, 1952. That alone makes this a major policy shift. But the real headline is not just the name change. It is the way the new scheme reshapes partial withdrawals, defining when members can access their funds and how much they are allowed to take.

At first glance, the changes may seem technical. Terms like “eligible member balance,” withdrawal ceilings, and minimum retained balance can sound like legal fine print. But don’t worry. Strip away the jargon, and the EPF New Rules 2026 are actually trying to do two things at the same time: give workers more flexibility today while protecting their retirement cushion for tomorrow.

Think of it like a water tank on your rooftop. You can draw water when you need it, but you cannot empty the tank completely every time there is a short-term need. Some water has to remain stored for the bigger days ahead. That is exactly how the new EPF withdrawal rule works.

In this article, we will break down the EPF Scheme 2026 withdrawal rules, eligibility, limits, conditions, and what they mean in practical, everyday language.

What Is the EPF Scheme 2026?

The EPF Scheme 2026 is the new framework notified by the Centre to replace the long-running EPF Scheme, 1952. This shift comes as part of the implementation of the Code on Social Security, 2020.

In plain English, this means the government has updated the legal and operational framework governing provident fund savings for employees. The old system had been around for decades. So, this is not a minor tweak. It is a structural update.

Why does that matter? Because EPF is not just another deduction on your salary slip. For many workers, it is one of the largest long-term savings pools they have. It acts as a safety net during retirement, but it also serves as a fallback option during emergencies, medical problems, housing needs, and major life events like education or marriage.

So when the rules change, employees need clarity. They need to know not only what is allowed, but also what is protected.

Why the New EPF Withdrawal Rules Matter

Let’s be honest. Most people do not read policy notifications for fun. They care when something affects their money. And EPF certainly does.

The revised rules matter because they directly affect how members can use their provident fund balance during critical moments in life. Need money for treatment? Planning higher education? Getting married? Buying a house? Leaving a job? The new rules set the boundaries for all these situations.

At the same time, the scheme is also trying to prevent members from draining their accounts too quickly. That is where the 25% minimum balance rule comes in. It acts like a protective wall around a part of your retirement savings.

In other words, the scheme says: yes, you can access your money for genuine needs, but no, you should not walk away with every last rupee if that puts your future at risk.

That balancing act is the heart of the EPF Scheme 2026.

The Biggest Change: The 25% Minimum Balance Rule

EPF Scheme 2026 Withdrawal Rules, If there is one rule that members absolutely need to remember, it is this one: you must maintain at least 25% of your eligible member balance in your EPF account.

This is the anchor of the new partial withdrawal framework.

What does that mean in simple terms? It means you cannot withdraw the full balance available in your account in most normal cases covered under partial withdrawal provisions. A quarter of the eligible balance must remain untouched.

This retained amount acts as a compulsory savings buffer. The idea is simple enough: life throws surprises, but retirement is still coming. If people withdraw too much too often, the long-term purpose of the provident fund gets weakened.

So, before calculating how much you can withdraw, the system first sets aside that mandatory 25%.

That is not just an accounting detail. It is the gatekeeper.

How the 25% Rule Works: A Simple Example

Let’s use the example mentioned in the source material because it explains the concept clearly.

Suppose an employee has an eligible member balance of ₹1 lakh in the EPF account.

Under the new rule:

- ₹25,000 must remain in the account

- The remaining ₹75,000 may be available for withdrawal, depending on the reason and the applicable conditions

This means that even when the rules say a member can withdraw “up to 100% of the eligible balance,” that calculation happens after the required minimum balance has been protected.

That is where many people may get confused. “Up to 100%” does not automatically mean “take out every rupee in the account.” It means up to 100% of the amount left after the minimum retained portion has already been set aside.

So yes, the wording may sound generous, but the structure remains cautious.

What Is ‘Eligible Member Balance’ Under the New Framework?

EPF Scheme 2026 Withdrawal Rules, The phrase “eligible member balance” is crucial under the revised EPF rules.

The scheme defines it as the amount available after deducting the compulsory 25% minimum balance. In other words, the system does not treat your total account balance as fully accessible for withdrawal. It first locks in the mandatory savings portion, and only then calculates what remains eligible.

This rule applies to both employee and employer contributions.

That point is important. Some members may assume only their own contribution is considered when applying the withdrawal rule. But the scheme makes it clear that the minimum balance requirement covers the combined structure of contributions.

So when you are trying to estimate how much you may actually receive, you cannot just look at the gross account balance. You need to factor in the protected amount that must stay behind.

It is a bit like having money in a fixed emergency fund at home. You may count it as part of your savings, but you do not treat it as spending money unless absolutely necessary.

Withdrawal for Medical Treatment: A Much-Needed Relief

Medical emergencies do not send calendar invites. They arrive suddenly, often when a family is least prepared. That is why the medical withdrawal provision under the EPF Scheme 2026 is one of the most important features in the revised rules.

Under the new framework:

- A member becomes eligible for medical-related partial withdrawal after 12 months of membership

- The member can withdraw up to 100% of the eligible balance

- The amount can be used for self or family members

This is significant because health-related financial pressure can become crushing very quickly. Hospital bills do not wait for payday, and insurance does not always cover everything. In such cases, EPF can function like a financial lifeboat.

Still, remember the 25% rule. Even in medical withdrawal cases, the eligible balance is calculated after the minimum amount is kept in the account.

So yes, members can access a substantial portion of their savings for treatment, but the system still preserves a core retirement reserve.

Withdrawal for Education: More Access, But With a Usage Limit

EPF Scheme 2026 Withdrawal Rules, Education expenses can feel like climbing a mountain with a backpack full of bricks. Tuition fees, books, accommodation, coaching, travel—the costs add up fast. The revised EPF rules recognize this reality.

For education-related withdrawals:

- A member must have completed 12 months of membership

- The member can withdraw up to 100% of the eligible balance

- This facility is allowed up to 10 times during membership

That last point matters. The scheme gives repeated access for education, but not without a ceiling. Ten withdrawals during membership is quite a wide window, which suggests the framework is trying to stay practical. After all, education is rarely a one-time cost. It may involve school fees, college admissions, professional courses, or other academic needs over time.

The provision offers flexibility, but it also nudges members toward responsible use. Just because the door is open does not mean it should be used casually. EPF is still a long-term savings instrument, not a day-to-day wallet.

Withdrawal for Marriage: Useful Support for a Major Life Event

Weddings are emotional, cultural, and, let’s face it, often expensive. Whether the expense is modest or lavish, marriage can place real financial pressure on households. The EPF Scheme 2026 continues to recognize marriage as a valid reason for partial withdrawal.

The revised rules state:

- Eligibility begins after 12 months of membership

- Members can withdraw up to 100% of the eligible balance

- The withdrawal is allowed up to 5 times during the membership of the fund

This provision gives members room to use their EPF savings for a major personal milestone. But the cap of five uses makes it clear that the facility is meant for specific life events, not routine withdrawals under the marriage label.

Here again, the structure is familiar: flexibility on one hand, discipline on the other. It is as if the scheme is saying, “We understand this is important, but let’s not forget why provident fund savings exist in the first place.”

Housing Withdrawal: One of the Most Practical Provisions

EPF Scheme 2026 Withdrawal Rules, If there is one area where EPF withdrawal can feel especially meaningful, it is housing. Buying or building a home is often the single biggest financial goal in a person’s life. And in India, owning a house still carries emotional weight far beyond bricks and cement. It means security. Stability. A place to belong.

Under the revised rules, housing-related withdrawals are allowed:

- After 12 months of membership

- Up to 100% of the eligible balance

- For a wide range of housing purposes

These housing purposes include:

- Buying a house or flat

- Purchasing a plot for construction

- Building a home

- Repaying a housing loan

- Carrying out repairs or improvements

This is a broad and practical list. It does not restrict housing support to just first-time purchase or construction. It also recognizes that homes need upkeep and that loan repayment can be a major burden.

That makes this provision especially relevant for working families. A person may need EPF support not only when purchasing property, but also when finishing construction, reducing loan stress, or making necessary repairs to an existing home.

In that sense, the housing rule is less like a single key and more like a toolbox.

Special Circumstances: A Flexible But Conditional Category

Not every financial hardship fits neatly into a labeled box. Life is messy. Some situations fall outside standard headings like treatment, education, or housing. That is where the special circumstances category under the EPF Scheme 2026 becomes important.

According to the revised rules:

- Members are eligible after 12 months of membership

- They may withdraw up to 100% of the eligible balance

- The request remains subject to approval under EPF rules

This is both helpful and cautious.

Helpful, because it creates room for situations that may not be cover under the main categories. Cautious, because the withdrawal is not automatic. Approval is still require under the applicable rules.

So, this is not a blank cheque. It is more like a safety valve built into the system. If an unusual but legitimate need arises, the framework allows for consideration—but not without oversight.

That kind of structured flexibility may prove useful for members facing circumstances that are serious, genuine, and difficult to classify.

Exit From Employment: A Key Relief Even Before 12 Months

EPF Scheme 2026 Withdrawal Rules, One of the more noteworthy features of the revised framework is the treatment of exit from employment.

In many withdrawal categories, the member must complete 12 months of membership before becoming eligible. But for employment exit, the rule is different.

Under the EPF Scheme 2026:

- A member may withdraw even before completing 12 months of membership

- The maximum allowed is up to 100% of the eligible balance

- A maximum of 2 withdrawals in a financial year is allowed

This is a practical response to workplace reality. Not every employee stays in one job for years. Some people leave due to layoffs, restructuring, health issues, relocation, family pressures, or simply because a job does not work out. In such moments, locking away all access to EPF savings until 12 months are completed could create hardship.

The revised scheme acknowledges that.

At the same time, it places a guardrail by allowing only two withdrawals in a financial year. That restriction helps prevent misuse while still offering support during a transition.

In simple terms, if job loss or employment exit hits like a storm, EPF is allowed to function as an umbrella—but not as something to be repeatedly opened and shut without limit.

How the New Rules Try to Balance Flexibility and Retirement Security

The smartest part of the EPF Scheme 2026 is not any single withdrawal category. It is the broader design philosophy behind them.

On one side, the scheme expands practical access. Members can use their funds for:

- medical treatment,

- education,

- marriage,

- housing,

- special circumstances,

- and even exit from employment.

On the other side, the scheme protects long-term retirement savings through the minimum 25% balance requirement.

That dual approach matters.

If the system allowed unrestricted access, many members might consume their future savings bit by bit, often for urgent but temporary needs. But if the system were too rigid, members would feel trapped, unable to use their own accumulated funds when life genuinely demands it.

The revised EPF framework tries to sit in the middle. It offers a controlled release of funds, not a free-for-all.

That may not satisfy everyone. Some employees may feel the 25% retention rule is too restrictive. Others may view it as necessary discipline. But either way, the intent is clear: provide support without destroying the retirement purpose of the fund.

What EPF Members Should Keep in Mind Before Applying for Withdrawal

Knowing the rules is one thing. Using them wisely is another.

Before making a withdrawal request under the EPF Scheme 2026, members should think through a few practical points.

First, understand your actual eligible balance, not just the total amount shown in your account. The 25% minimum balance has to remain, so the accessible amount may be lower than you expect.

Second, check the reason-based eligibility condition. Most categories require 12 months of membership, while employment exit can apply even earlier.

Third, be mindful of frequency limits. For example:

- Education withdrawals are allowed up to 10 times

- Marriage withdrawals are allowed up to 5 times

- Exit from employment allows 2 withdrawals in a financial year

Fourth, remember the purpose of EPF itself. This is not meant to replace regular savings, emergency funds, or monthly budgeting. It is a long-term financial support structure. Using it occasionally for real need makes sense. Depending on it too often may weaken your future safety net.

In short, a withdrawal may be allow under the rules, but that does not always mean it is the best first option.

Common Confusion Around ‘Up to 100% Withdrawal’

EPF Scheme 2026 Withdrawal Rules, One phrase in the revised framework may easily confuse readers: “up to 100% of the eligible balance.”

At first hearing, it sounds like full access. But that phrase needs to be read carefully.

The word that matters most is not “100%.” It is “eligible.”

Because the eligible balance is calculate after removing the mandatory 25% retained amount, the actual withdrawable amount is lower than the total account balance.

So if a member assumes, “I can take all the money from my EPF account,” that may not be correct under the partial withdrawal framework described here.

This distinction is not just technical—it is central. Missing it could lead to unrealistic expectations and confusion at the time of withdrawal.

If you remember only one sentence from this section, let it be this: 100% withdrawal is allow only on the eligible portion, not automatically on the full EPF balance.

Why Housing and Medical Withdrawals May Matter Most for Families

Among all the listed withdrawal reasons, two stand out for everyday household relevance: medical treatment and housing.

Why these two? Because both can create sudden and heavy financial pressure. A medical emergency can drain savings in days. A housing purchase or loan burden can shape a family’s finances for years.

The revised rules recognize that by allowing withdrawals of up to 100% of the eligible balance in both categories, subject to the framework’s conditions.

For a middle-class family, this could make a big difference. It can mean faster access to treatment money without taking on crippling debt. It can mean support with buying a flat, repaying a home loan, or repairing a home that has become unsafe or inadequate.

That does not make EPF a substitute for insurance or planned housing finance. But it does make it a meaningful fallback reserve.

And sometimes, that reserve is what keeps a financial setback from becoming a crisis.

How the EPF Scheme 2026 Reflects a More Modern Approach

The move from the EPF Scheme, 1952 to the EPF Scheme 2026 is not just about updated paperwork. It signals a more modern way of thinking about worker savings.

Today’s workforce is different from that of the 1950s. Jobs change faster. Family structures are shifting. Education costs are rising. Healthcare demands are more complex. Housing is more expensive. Mobility between employers is more common.

A rigid savings framework designed for another era would struggle to keep up.

The revised scheme appears to acknowledge that reality. It does not abandon the original retirement purpose of EPF, but it does try to make the fund more responsive to real-life needs.

That is perhaps the most important takeaway. The scheme is not simply loosening rules. It is redesigning access while preserving restraint.

It is less like opening the floodgates and more like building smarter channels.

A Quick Snapshot of Withdrawal Reasons, Eligibility and Limits

To make things easier, here is the revised withdrawal framework in plain language:

- Medical treatment: Eligible after 12 months; up to 100% of eligible balance; for self or family

- Education: Eligible after 12 months; up to 100% of eligible balance; can be use up to 10 times

- Marriage: Eligible after 12 months; up to 100% of eligible balance; can be use up to 5 times

- Housing: Eligible after 12 months; up to 100% of eligible balance; can be use for purchase, construction, loan repayment, repair or improvement

- Special circumstances: Eligible after 12 months; up to 100% of eligible balance; subject to approval

- Exit from employment: Can apply even before 12 months; up to 100% of eligible balance; maximum 2 withdrawals in a financial year

And across these provisions, one golden rule remains in place: 25% of the eligible member balance must stay in the EPF account.

What Employees Can Learn From the Revised Framework

So, what is the practical lesson here for EPF members?

It is this: your EPF account is no longer just a locked retirement box. Under the revised framework, it is also a structured support system for major life needs. But it comes with boundaries designed to stop short-term needs from swallowing long-term security.

That balance is important. Too much access can be risky. Too little access can be unfair. The EPF Scheme 2026 tries to bridge that gap.

For employees, the smart move is to treat EPF as a strategic reserve. Use it when the reason is genuine and the timing is right. Understand the limits. Respect the long-term purpose of the fund. And do not confuse flexibility with unlimited freedom.

After all, retirement savings are a bit like planting a tree. You may trim a few branches when necessary, but you do not cut down the trunk if you still want shade in the future.

Read More: EPF Withdrawal Through UPI: How PF Money Could Become Instantly Accessible

Conclusion

EPF Scheme 2026 Withdrawal Rules, The EPF Scheme marks a significant shift in how provident fund savings can be accessed and protected. By replacing the older 1952 framework, the new system introduces more practical withdrawal options for medical treatment, education, marriage, housing, special situations, and even employment exit. At the same time, it draws a firm line through the 25% minimum balance rule, ensuring that members do not empty out their retirement nest egg too easily. The result is a more flexible yet disciplined approach—one that tries to support workers through life’s big moments without losing sight of long-term financial security.

If there is one simple way to read the new EPF withdrawal rules, it is this: the scheme gives you room to breathe, but not room to burn through your future. For EPF members, that makes understanding these rules not just useful, but essential.