Pension Tax Rules, Retirement is supposed to be the phase of life where people finally relax, enjoy their savings, and spend more time with family. But every tax season, many pensioners find themselves tangled in confusion over one simple question: how exactly is pension taxed?

It may sound straightforward, but under India’s Income-Tax Act, pension and family pension are treated very differently. And believe it or not, this single distinction can completely change how your income is taxed, what deductions you can claim, whether TDS applies, and even whether you need to file an Income Tax Return (ITR) at all.

As filing for Assessment Year (AY) 2026-27 gains momentum, understanding pension tax rules and family pension taxation has become more important than ever. With the Income Tax Department increasingly using AI-driven systems and automated data matching, even small reporting mistakes related to pension income or family pension taxation can trigger notices, refund delays, or unnecessary scrutiny.

So, let’s break it all down in simple language.

Why Pension Is Still Treated as Salary After Retirement

Here’s something many retirees don’t realize: retirement does not change the nature of pension income.

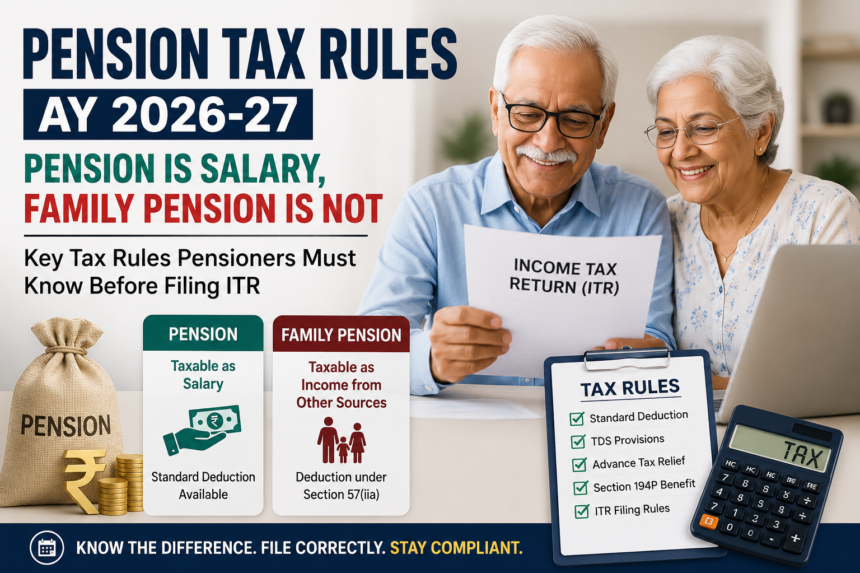

Under Section 17(1) of the Income-Tax Act, pension is considered a continuation of salary because it arises from the employer-employee relationship that existed before retirement. In simple words, your pension is basically deferred compensation for services you rendered during your working years.

That’s why pension income is taxed under the head:

“Income from Salaries”

Think of it like an echo of your monthly paycheck. Even though you’re no longer working, the income still carries the “salary” tag in the eyes of tax authorities.

And this classification comes with benefits.

Standard Deduction Available to Pensioners

Pension Tax Rules, Since pension is taxed as salary income, pensioners are eligible for the standard deduction under Section 16(ia).

This deduction helps reduce taxable income without requiring any investment proof or expense documentation.

Under the Old Tax Regime

- Standard deduction allowed: Rs 50,000

- Or the amount of pension, whichever is lower

Under the New Tax Regime

- Standard deduction allowed: Rs 75,000

- Or the amount of pension, whichever is lower

For many retirees who rely heavily on pension income, this deduction can significantly reduce tax liability.

Imagine it as a built-in tax cushion that softens the impact of taxation after retirement.

Family Pension Is a Completely Different Story

Now comes the part where most taxpayers make mistakes.

Family pension is not treated the same way as regular pension.

When a spouse, child, or legal heir receives pension after the death of a pensioner or employee, the Income-Tax Act does not consider it salary income. Why? Because the recipient never had an employer-employee relationship with the pension-paying authority.

As a result, family pension is taxed under:

“Income from Other Sources” under Section 56

That small change in classification makes a huge difference.

And here’s the catch many people miss: family pensioners cannot claim the standard deduction available to salaried individuals and pensioners.

What Deduction Can Family Pensioners Claim?

Pension Tax Rules, Although standard deduction is not available, family pensioners do get relief under Section 57(iia).

But the deduction structure is different.

Under the Old Tax Regime

Deduction allowed is:

- One-third of family pension, or

- Rs 15,000

- Whichever is lower

Under the New Tax Regime

Deduction allowed is:

- One-third of family pension, or

- Rs 25,000

- Whichever is lower

This distinction is extremely important during ITR filing.

If a taxpayer incorrectly reports family pension as salary income, it may lead to excess deduction claims and incorrect tax computation. That can invite notices from the Income Tax Department later.

Pension vs Family Pension: The Biggest Tax Differences

Let’s simplify the comparison.

Regular Pension

- Taxed as salary income

- Covered under Section 17(1)

- Eligible for standard deduction

- TDS deducted under salary provisions

- Employer-employee relationship exists

Family Pension

- Taxed as income from other sources

- Covered under Section 56

- Standard deduction not allowed

- Deduction available under Section 57(iia)

- No employer-employee relationship exists

It’s like comparing apples and oranges. They may look similar on the surface, but tax laws treat them very differently.

Senior Citizens Get Relief from Advance Tax

Here’s some good news for senior citizens.

Under Section 207(2), resident individuals aged 60 years or above are exempt from paying advance tax if they do not have income from business or profession.

This benefit applies to both pensioners and family pensioners.

Conditions for Advance Tax Exemption

The individual must:

- Be a resident in India

- Be aged 60 years or above

- Not have business or professional income

This means many retirees can avoid the stress of quarterly advance tax payments.

However, don’t misunderstand the relief.

The exemption only applies to advance tax payments — not to the tax itself. Any remaining tax liability must still be paid while filing the ITR as self-assessment tax.

The silver lining is that eligible senior citizens can avoid interest penalties under Sections 234B and 234C for non-payment of advance tax.

TDS Rules for Pension and Family Pension

Pension Tax Rules, Another major area of confusion is Tax Deducted at Source (TDS).

TDS on Pension

Since pension is treated as salary income, banks or pension-paying authorities deduct TDS under Section 192.

The deduction is calculated after considering:

- Standard deduction

- Tax regime selected

- Eligible rebate

- Other applicable deductions

So, pensioners usually receive pension after tax deduction.

TDS on Family Pension

Family pension works differently.

There is no specific TDS provision applicable to family pension under the Income-Tax Act. That means family pension is generally paid without TDS deduction.

But here’s where people get trap.

No TDS does not mean tax-free income.

Family pension remains taxable, and taxpayers may suddenly discover a tax liability while filing returns because no tax was deducted during the year.

It’s similar to driving without seeing speed breakers ahead — the impact comes later.

Section 194P: A Massive Relief for Very Senior Citizens

Pension Tax Rules, The government has also introduced a major compliance relief for elderly pensioners.

Under Section 194P, certain very senior citizens are exempt from filing income-tax returns altogether.

Who Can Claim This Benefit?

The individual must:

- Be a resident in India

- Be age 75 years or above

- Have only pension income and interest income

- Earn interest from the same bank where pension is receive

- Submit Form 12BBA to the specified bank

Once the declaration is submit, the bank itself calculates taxable income after considering:

- Chapter VI-A deductions

- Rebate under Section 87A

- Applicable tax liability

The bank then deducts the required TDS.

After this process, the individual is not require to file an ITR under Section 139.

For elderly citizens who struggle with paperwork or online filing systems, this provision acts like a welcome breathing space.

Why Correct Classification Matters More Than Ever

Gone are the days when minor filing mistakes slipped through unnoticed.

Today, the Income Tax Department relies heavily on:

- AI-driven compliance systems

- Automated data matching

- AIS verification

- Form 26AS reconciliation

- Pre-filled ITR data

That means incorrect reporting of pension income can quickly create mismatches.

For example:

- Reporting family pension as salary income

- Claiming wrong deductions

- Ignoring taxable family pension

- Misreporting TDS details

These mistakes can lead to:

- Tax notices

- Refund delays

- Additional tax demands

- Compliance scrutiny

In short, accuracy matters more than ever before.

Documents Pensioners Must Verify Before Filing ITR

Pension Tax Rules, Before submitting returns for AY 2026-27, pensioners should carefully cross-check all financial documents.

Important Documents to Review

- Form 16 or pension statement

- AIS (Annual Information Statement)

- Form 26AS

- Bank interest certificates

- Pre-filled ITR data

Even one mismatch can create complications later.

Think of these documents as puzzle pieces. If one piece is misplace, the entire picture can appear incorrect to the tax department.

Common Mistakes Pensioners Should Avoid

Many taxpayers unknowingly make errors while filing returns.

Most Common Pension Filing Mistakes

- Reporting family pension under salary income

- Claiming standard deduction on family pension

- Ignoring taxable bank interest

- Forgetting self-assessment tax payment

- Choosing the wrong tax regime

- Not reconciling AIS and Form 26AS

Avoiding these mistakes can save pensioners from unnecessary headaches.

The Bigger Message for Pensioners in AY 2026-27

The golden rule is simple:

Pension is salary. Family pension is not.

This one distinction determines:

- The correct income head

- Eligibility for standard deduction

- Deduction under Section 57(iia)

- TDS applicability

- Tax calculation

- Return filing obligations

And in an era of digital tax scrutiny, getting these details right is no longer optional.

For retirees, tax compliance today is not just about saving money. It’s equally about staying stress-free, avoiding notices, and ensuring timely refunds.

Read More: LIC Bonus Issue 2026: Shares Rally After Insurer Announces Historic 1:1 Bonus

Conclusion

Pension Tax Rules, Tax rules for pensioners may appear confusing initially, but once you understand the difference between pension and family pension, everything becomes much clearer.

Regular pension continues to enjoy the status of salary income, along with the valuable benefit of standard deduction. Family pension, on the other hand, falls under income from other sources and follows an entirely separate deduction framework.

Senior citizens also enjoy several important reliefs, including exemption from advance tax and, in some cases, exemption from filing ITR itself under Section 194P.

As AY 2026-27 filing season progresses, pensioners must pay close attention to proper income classification, deduction eligibility, TDS treatment, and document verification. A careful and informed approach today can help avoid tax notices, disputes, and refund delays tomorrow.

Ultimately, understanding pension taxation is not just about compliance — it’s about protecting financial peace of mind during retirement.