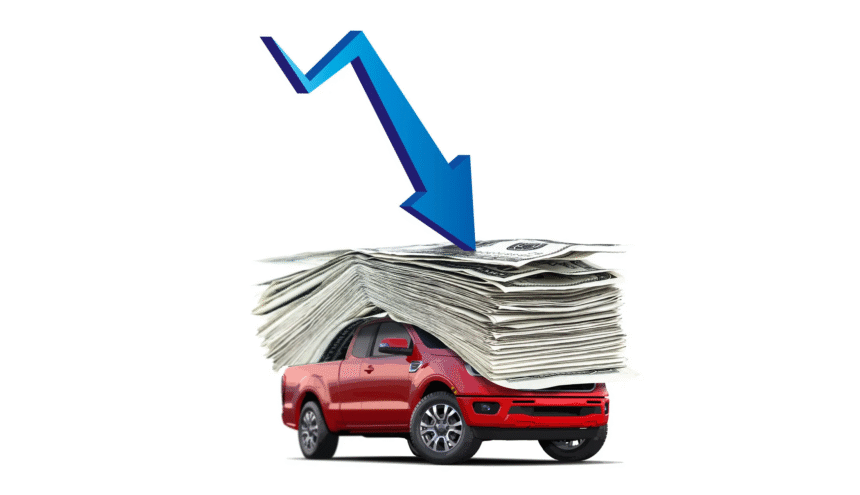

Buying a new car can be one of the most exciting milestones in life. Whether its your very first vehicle or an upgrade to something more reliable, owning a car often symbolizes independence, freedom, and progress. However, what many new buyers may not realize is that the financing structure behind their dream purchase could lead them into financial challenges down the road. One of the biggest pitfalls in auto financing is something called a negative equity auto loan.

In simple terms, negative equity means you owe more on your car loan than the car is actually worth. This can create a chain of financial stress, limit your options for refinancing, and even put you at risk of long-term debt.

In this article, well dive deep into what negative equity auto loans are, why they happen, and how they can impact you as a new buyer. Well also explore the role of auto equity loans, how to calculate your equity, and how to avoid falling into the trap of owing more than your vehicles value.

Understanding Auto Equity and Auto Equity Loans

Before exploring the dangers of negative equity, lets first define auto equity.

-

Auto equity is the difference between the current market value of your car and the amount you still owe on your auto loan.

-

If your car is valued at $20,000 and you owe $10,000, you have $10,000 in positive equity.

-

But if your car is worth $15,000 and you still owe $18,000, youre in negative equitysometimes referred to as being upside down on your loan.

An auto equity loan allows you to borrow against the positive equity of your car. For example, if you own your car outright or owe very little compared to its value, you can use your vehicle as collateral to obtain a loan. Many people search for auto equity loan near me to find local lenders who can provide quick cash based on their vehicles value.

However, while auto equity loans make sense for those with strong equity, buyers with negative equity auto loans dont have this option. Instead, theyre stuck in a situation where their car loan is costing more than their vehicle is worth.

The Problem of Negative Equity Auto Loans

So why do negative equity auto loans exist in the first place? It often boils down to how new cars depreciate.

Rapid Depreciation

A brand-new car can lose 10% to 20% of its value in the first year alone. By the end of year three, it may have lost over 30% of its original value. If you buy a car with little or no down payment, the chances of being in negative equity are high from day one.

Long-Term Financing

Dealerships often advertise enticing monthly payments that feel affordable. However, these low payments usually come from stretching the loan termsometimes up to seven or eight years. While this reduces the monthly burden, it also means you pay interest longer, and your principal balance decreases very slowly. In many cases, the cars value falls faster than your loan balance.

Rolling Over Old Debt

Another factor is when buyers trade in cars that already have negative equity. Many dealers will roll that debt into the new loan, meaning you start off owing much more than the car is worth.

Why Negative Equity Auto Loans Are Dangerous

Being in a negative equity situation can affect more than just your wallet. For new buyers especially, the financial impact can be overwhelming.

1. Limited Flexibility

If you need to sell or trade your car, you wont be able to do so without taking a loss. For example, if your loan balance is $22,000 but your cars value is only $18,000, selling the vehicle means youll still owe $4,000 out of pocket.

2. Higher Risk of Repossession

If unforeseen circumstances make it difficult to keep up with payments, your options are slim. Defaulting may lead to repossession, and youll still be responsible for the balance after the lender sells the car at auction.

3. Difficulty Refinancing

Refinancing works much better for positive equity car loans. If youre upside down, lenders are wary of extending better terms, since the collateralthe caris already worth less than what you owe.

4. Strain on Your Credit and Future Borrowing

Carrying a negative equity auto loan affects your overall debt-to-asset ratio, which can in turn lower your borrowing power for future needs like mortgages or personal loans.

How to Calculate Your Equity

The good news is you can track and calculate your equity status to avoid surprises. Here are the steps:

-

Find your loan balance Check your lenders online portal or latest statement to see exactly how much you owe.

-

Determine your cars value Use trusted resources such as Kelley Blue Book (kbb.com) or Edmunds to get a fair market value for your car.

-

Subtract loan balance from car value If the result is positive, you have auto equity. If its negative, you owe more than the car is worth.

There are also tools like an auto loan calculator with negative equity that can help you simulate outcomessuch as how rolling over debt into a new loan affects your payments and overall equity position.

How to Avoid Falling Into Negative Equity

Especially for new buyers, avoiding a negative equity trap requires planning. Some practical ways include:

-

Make a larger down payment. Aim for 20% or more if possible. This reduces your loan balance right away and helps balance out early depreciation.

-

Avoid excessively long loan terms. A 5-year loan is a good balance; anything longer increases the risk of negative equity.

-

Research cars with higher resale value. Some brands depreciate faster than otherschoosing a vehicle with strong reliability and demand helps protect your equity.

-

Dont roll old debt into a new loan. While this seems convenient, it often locks you into years of financial imbalance.

-

Pay more than the minimum payment. Extra payments on your principal loan balance help reduce risks by accelerating equity growth.

The Role of Auto Equity Loans Today

For individuals with positive equity, an auto equity loan can be a smart financial tool. These loans may come with lower interest rates compared to unsecured personal loans, since the vehicle acts as collateral. They are often used for emergencies, debt consolidation, or covering unexpected expenses.

If youre searching for an auto equity loan near me, make sure to compare lenders carefully. Look at repayment terms, fees, and interest rates. Most importantly, only borrow against your equity if you are confident you can manage repayment.

Key Takeaways for New Buyers

-

Understand what youre signing up for. A negative equity auto loan can trap you in years of unbalanced debt.

-

Use tools wisely. An auto loan calculator with negative equity is invaluable for forecasting financial outcomes before signing any deal.

-

Leverage positive equity when possible. If your car holds value, you can tap into it through an auto equity loan instead of piling on debt.

-

Think long-term. Dont just focus on the monthly paymentconsider total cost, depreciation, and resale value.

Read More: Auto Equity Loans vs. Title Loans: Which Is Safer?

Conclusion

While owning a vehicle is nearly essential in todays fast-paced world, how you finance that vehicle matters just as much as the type you choose. A negative equity auto loan may seem manageable at first, but it often hides financial risks that surface when life circumstances change. For new buyers especially, avoiding negative equity requires discipline, research, and smart financial decisions.

By making a significant down payment, keeping loan terms reasonable, avoiding debt rollovers, and tracking your equity regularly, you can protect yourself from falling into a cycle of debt. On the other hand, those with positive equity can explore auto equity loans responsibly as a way to access funds without jeopardizing financial stability.

When it comes to buying a car, remember: its not just about getting the keysits about keeping your financial health intact long after you drive off the lot.

Authoritative resource for vehicle valuation and finance tools: Visit Kelley Blue Book to check accurate car values, resale trends, and financing calculators helpful for managing auto equity.